Valuation: What is your company worth?

Valuation is the process of determining what your company is worth. In the M&A process, it is often performed ahead of going to market.

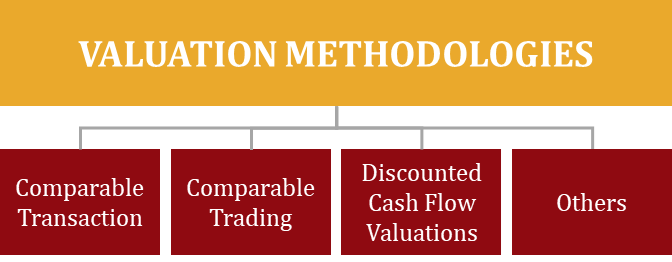

VALUATION METHODOLOGIES

There are three primary valuation methodologies: 1) comparable transaction multiples, 2) comparable trading multiples, 3) and discounted cash flow analysis. There are also other types of valuation methods that are not as relevant to middle-market M&A; therefore, this blog will focus on the three main ones.

Comparable Transaction Multiples

Comparable transaction valuations refer to what the market has offered for companies comparable to the company being evaluated. For example, if a company sold at eight times EBITDA, it’s logical to assume that another similar company would trade at eight times EBITDA. The multiple will depend on various attributes of the specific target company, such as whether it is growing faster or slower, whether the management team is better or worse, client concentration, or geographic concentration, etc. Many things influence the multiple that a buyer is willing to pay.

Comparable Trading Multiples

Comparable trading multiples involves looking at where the comparable public companies are trading. The comparable trading valuation metrics are a little more theoretical for the middle market transactions. It is a helpful metric and something used in negotiations with buyers, but there are all sorts of factors that drive the multiple relative to what you might expect to achieve in the private market. For example, volatility in the public market will impact the valuation of public companies. You do not see the same day-to-day volatility in a private transaction. Also, for middle-market companies, comparable trading valuation is less relevant because of the size differential and the liquidity.

Discounted cash flow

The discounted cash flow valuation is an analysis of the business’ free cash flows. The cash flows are discounted at a certain discount rate to arrive at the net present value. The biggest drivers of this analysis include the discount rate, which could be derived using the CAPM model, and various other factors. This method is more relevant to the question, “What is my company worth to me?”, not necessarily what it’s worth to someone else.

WHAT MULTIPLES SHOULD I LOOK AT?

Aside from the valuation methodologies, the other important piece is what multiple metrics to use. Generally, the two main metrics are EBTIDA and revenue multiples.

Revenue Multiple

Revenue multiples are generally used for pre-profitability companies. It is often used in high-growth type businesses such as software and biotech companies and recurring revenue companies. The revenue multiples range depending on the industry.

EBITDA Multiple

EBITDA is a proxy for cash flow and normalizes income between various companies and is generally used for more mature companies.

There are many different metrics that buyers and sellers can focus on, and it is always industry-specific. Also, there are a lot of different ways to define what the metric is. Some industries use GAAP accounting, and some use some special purpose accounting.

OTHER VALUATION CONSIDERATIONS

Add backs

Add backs to EBITDA help demonstrate what the company’s earnings stream looks like going forward. It involves adjusting historical EBITDA for known future or recent arrangements, such as one time expenses or increased operating efficiency.

Synergy

Synergy can be created when two companies combine, and instead of being one plus one equals two, one plus one equals three. That could be because of expense reductions or revenue enhancements. Buyers will benefit from synergies in the future. A competitive process will increase the likelihood that a seller will get paid for at least a portion of the synergies a buyer may achieve.

Customer Concentration

Customer concentration or any distribution channel concentration will typically reduce valuation multiples. Customer concentration typically entails any single customer greater than 15%.

WHAT IS YOUR COMPANY WORTH?

Ultimately, it is the market that sets the transaction price—your company is worth whatever someone is willing to pay for it. The real value of hiring a financial advisor to help sell a business is to get the best price and terms, which are generally achieved through a carefully managed auction process.

For more on company valuation, listen to the Middle Market Mergers & Acquisitions podcast episode 012: What is my company worth? here https://coladv.com/podcasts/012-what-is-my-company-worth/

Related Posts: