In this episode, Gina Cocking and Jeff Guylay continue their discussion on deal structuring.

Today, we explore rollover equity, a form of contingent consideration in which the seller takes a portion of its proceeds as equity ownership of the new or acquiring company. In this episode, we cover:

- Why is rollover equity important?

- How often is it used?

- How is it structured?

- What happens in platform investments vs smaller add ons?

- How does it differ from management incentive pools and from taking stock as consideration in a publicly traded company?

We talked about how the math works related to rollover equity in leveraged transactions and how we help manage these critical negotiations with buyers. Importantly, we talked about how rollover equity can set up all parties in the transaction for success through the alignment of interests.

Other episodes in our series about deal structuring include price and terms, earn outs, R&W insurance, and roll ups.

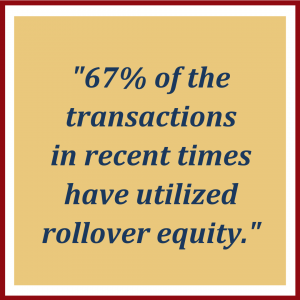

More than two-thirds of M&A transactions in recent times utilize rollover equity. The primary purpose of rollover equity is to align interests through shared economic ownership. Rollover equity gives the owner a second bite at the apple, as you’ll hear in the episode and read in the show notes. Rollover equity is also tax-deferred.

Later in the episode, Jeff is joined by our guest Vernon Rew, a partner at Whitaker, Chalk, Swindle & Schwartz, who shares his perspective on closing conditions and the importance of staying on task and getting deals to the finish line.

In this episode, Colonnade Advisors addresses the following questions as related to rollover equity:

What is rollover equity? (00:55)

Gina: “The sellers of the company, the founders, the owners are going to take some of their proceeds and roll it over into equity and ownership of what we call Newco. Newco is the new or acquiring entity.”

Why is rollover an important equity component of a transaction? (01:52)

Jeff: “Probably the most important answer or topic here is that it aligns interests, particularly when you’re talking to private equity-backed buyers.”

How often is rollover equity used in transactions? (02:56)

Gina: “67% of the transactions in recent times have utilized rollover equity.”

What are the tax implications of rollover equity? (05:10)

Gina: “Taking equity as consideration in a deal is tax-deferred. With equity that you are rolling over, no taxes are paid at the closing. You’re not going to pay taxes until you sell that equity and convert it into cash.”

What are the other advantages of rollover equity? (05:55)

Gina: “Another advantage of rollover equity is that it gives the owner a second bite at the apple. Rollover equity can be valuable. With that second bite at the apple, we have seen many cases of people that have gotten very wealthy with the second turn of the sale of the business, and even third turn.”

What is the seller demonstrating to the buyer when rolling over equity? (08:40)

Jeff: “Showing commitment and confidence in the forecast and the business, and just setting up the business for success through mutual understanding.”

What is the role of a financial advisor, such as Colonnade, in rollover equity discussions? (09:30)

Gina: “Rollover equity introduces a whole other component to diligence where it’s the diligence of the other side. That is where a trusted advisor’s perspective is helpful. In our case, with many of our clients on the deals we work on, we know the universe of potential buyers pretty well, so we can give our perspective.”

If selling the business to a private equity firm as a platform company, what type of diligence should be performed? (10:15)

Jeff: “There is due diligence around the private equity firm and their experience and track record. The dating dynamics of some of these management meetings are fundamental because these are going to be your partners.”

If selling the business to a private equity-backed strategic company, what type of diligence should be performed? (10:47)

Jeff: “You have to conduct due diligence and relative valuation on this private equity-backed firm that already exists and has operations and that already has a set private market valuation.”

How is rollover equity different from stock options and incentive pools? (12:05)

Gina: “Stock options and incentive pools are subjective decisions by the board as to what you get for hitting certain performance goals. It is very different. Rollover equity is your property, and you have property rights to it. They cannot take that away.”

Are there restrictions on what the seller can do with the rollover equity? (13:01)

Jeff: “There are almost certainly going to be restrictions around what you can do with the stock. The operating agreement that your attorneys will help you review, and you’ll sign onto, will typically have pretty strict covenants related to how you can dispose of the stock.”

What type of securities are used with rollover equity? (15:45)

Gina: “Our goal is to get pari passu, meaning the same type. We make sure in deals today that the sellers get the same type of equity as the buyers. If the buyers are getting preferred, we want the sellers to get preferred.”

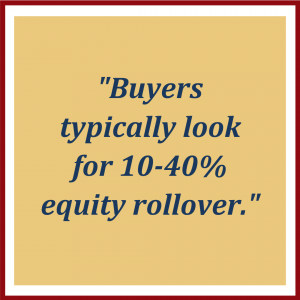

Typically, what percentage of the total transaction consideration is rolled over? (18:12)

Gina: “It’s a complicated question. Buyers typically look for 10%-40% equity rollover. It depends on who the buyer is. Private equity buyers will probably want to see a lot of rollover equity. Buyers look at it as a core part of their strategy to incentivize everyone.”

How do rollover equity considerations differ if the buyer is a public company? (19:40)

Jeff: “With public companies, the discussion is usually different. It can be a tax discussion. It is a separate analysis. The thesis is the same, but it is used really for other purposes.

When do rollover equity discussions typically take place in a transaction? (20:45)

Jeff: “We usually have it as one of the near-final conversations with the buyer that we select in exclusivity.”

How is the seller’s rollover equity percentage ownership of the new company determined? (22:47)

Gina: “It is based on the equity value of the new or acquiring company and depends on the leverage in the transaction. The percentage of your rollover proceeds does not necessarily equate to the percentage of the new company ownership.”

What are the benefits of using a financial advisor in rollover equity discussions between the seller and buyer? (25:50)

Jeff: “Our experience in working with these types of transactions is powerful in terms of making sure that they get done well for the seller. Otherwise, these things can blow up pretty quickly if you just put people in a room and start talking about rollover equity.”

What effect does any additional equity grants or incentives for employees have on the seller’s equity rollover percentage ownership of the company? (26:48)

Jeff: “There’ll be diluted pro-rata just like everyone else. The sellers and buyers have locked arms, and they are in the same security and position. Any additional equity grants or incentives will dilute everyone on a pro-rata or equal basis.”

Will current sellers of the company be asked to rollover equity at the next transaction? If so, why? (27:06)

Gina: “Current sellers of the company – who are important to the ongoing operations of the business – may have to rollover equity again in the future at the next transaction. For example, a private equity firm has bought your company, and you rolled over equity. The private equity firm then sells the company to another private equity firm in the future. The new owner would like to see you be equally incentivized or have skin in the game and would like to have some equity rollover.”

Can the owner completely exit the business after a few years post-transaction? (28:52)

Jeff: “That is usually a good conversation to have with buyers as long as we’re clear and upfront about it. We want to make sure that everyone knows that the management transition plan has to start immediately. You have to be in a position where you’ve got the next set of leaders up and ready for the next transaction, whether it’s one, three, or five years.”

Jeff invites Vernon Rew, a partner at Whitaker, Chalk, Swindle & Schwartz, to share his perspective on closing conditions in a transaction.

What closing conditions do you see in M&A transactions, and why are these conditions so important?

- Closing conditions are critical because if a single closing condition is not met, you’re likely not closing

- It is important to obtain all necessary third-party consents and all required regulatory approvals

- The material adverse effect and the material adverse change provisions are essential and often highly negotiated

- Focusing on the process and keeping all members of the seller team on task and focused on getting to the close are critical

- Time is critical. A delay in completing a closing consideration could kill a deal

Featured guest bio and contact information:

Vernon Rew

Email: vrew@whitakerchalk.com

Vernon Rew has over 35 years of legal experience representing business clients in corporate matters, contract negotiations, mergers and acquisitions transactions, and securities law compliance matters. Vernon has represented both public companies and privately held entities in a wide variety of industries.

Vernon’s mergers and acquisitions practice has included representation of both sellers and buyers in a large number of transactions throughout his career. He has worked in a wide range of manufacturing and service industries in his corporate and contracts negotiating practice. In his securities law compliance practice, he has counseled clients with SEC filings, tender offers, public offerings, and going private transactions. Vernon considers himself a relationship lawyer and is an experienced counselor and negotiator on behalf of his clients.