In this episode, Gina Cocking and Jeff Guylay continue their discussion around the due diligence process related to the sale of a company.

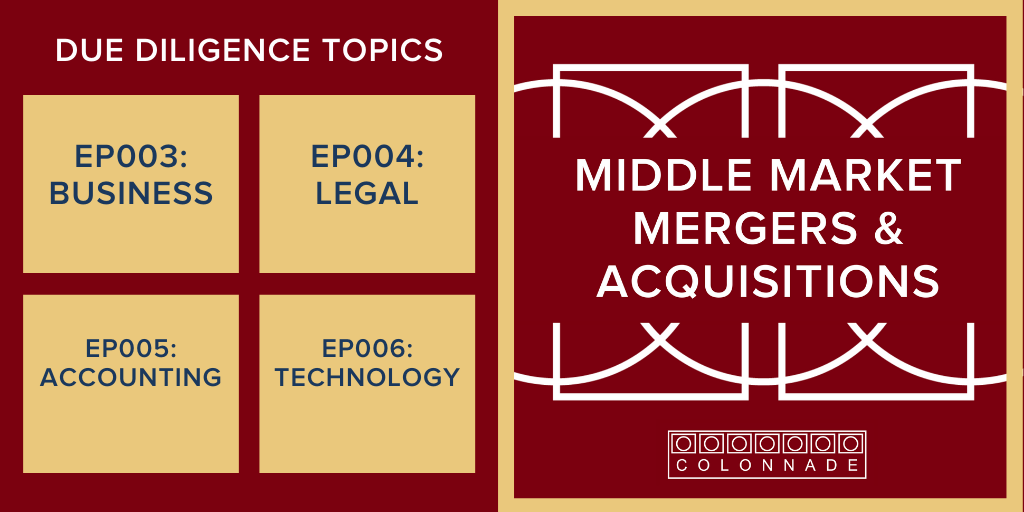

This episode is part of a four-episode series exploring the due diligence process that began with 003 on the business aspects of the due diligence process.

EP003: Business aspects of due diligence

EP004: Legal aspects of due diligence

EP005: Accounting aspects of due diligence (today’s episode)

EP006: Technology aspects of due diligence

In today’s episode, we invite our featured guest, Joe Kaczmarek, to share his insights on how companies can best prepare for an M&A transaction. Joe is the National Fintech practice leader at RSM, a leading provider of audit, tax, and consulting services focused on the middle market.

There are six key takeaways from the episode (35:17)

- Start early

- Review your financials monthly

- Keep books in GAAP (Generally Accepted Accounting Principles)

- Get an audit

- Prepare forecasts for your business and track achievement to forecast

- Invest in the finance department. If your goal is to sell your company, the number one action you should take (related to accounting and finance due diligence) is to get a good CFO

In this episode, Colonnade Advisors addresses the following questions as related to the accounting aspects of due diligence:

When should an owner start preparing to sell their company? (01:20)

Gina: “It starts years in advance. At the very basic level, a business owner or leader of a company should be reviewing the financials on a monthly basis. The reason is to get comfortable with the cadence of their business so that they can talk to the financials.”

Does a company need a public audit prior to selling the company? (1:40)

Gina: “We recommend all companies have a financial audit for several years before they go to market.”

What is the difference between an audit and a compilation? (01:58)

Gina: “A compilation is when accountants come in and put your financials together for you. They may even do it on a GAAP basis. An audit means that the accounting firm is doing a deep dive into the numbers. They’re looking at bank reconciliations. They’re doing different types of testing for fraud and for receivables and payables, et cetera. It’s a very involved process, but it is a must for a business that is planning for a successful sale.”

Do I need a financial forecast? (02:35)

Gina: “A company should keep a forecast and measure themselves to the forecast and plan. The reason for this is twofold: 1) I believe that you only get to where you’re going if you plan for it, and 2) buyers are going to look at the company’s financial forecast and how they are doing compared to that forecast.”

What other financial statements must be in order? (03:54)

Gina: “Another good thing to prepare for a sale process is a monthly data book. This data book includes the income statement, cash flow statement, balance sheet, and MD&A (Management Discussion and Analysis).”

How does a company select an accounting firm to work with on accounting due diligence? (06:25)

Gina: “I usually recommend that companies not go with the local firm that does their tax returns. Typically (I recommend) a regional accounting firm, or a national one, because you need a team that can defend its choices in accounting principles interpretation.”

When should a company start working on accounting due diligence? (08:20)

Jeff (07:37): “The sooner the better. The first audit is the worst. After that, it gets a little bit easier. Getting that process rolling is important.”

When is meeting the financial forecast key? (10:21)

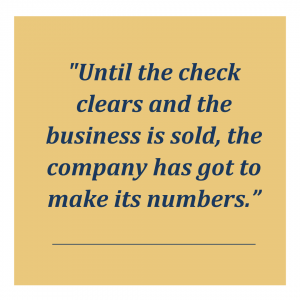

Gina: “The financial forecast is crucial when we’re actually selling the business. The key is when you’re in the sale process, from the moment we release that confidential information memorandum (CIM) until the check clears and the business is sold, the company has got to make its numbers.”

What is the management team’s role in owning the forecast? (11:44)

Jeff: “It’s important that the management team understands and owns the forecast because they’re going to have to live with it. The financial forecast obviously develops the metrics upon which you’re going to be judged either through management contracts, earn outs or just general performance. You really want to be confident that you’re going to hit the numbers one, two, three years out.”

What is an MD&A (Management Discussion and Analysis)? (13:45)

Gina: “A paragraph or a page and a half that explains the numbers, e.g. ‘Revenues were up by X because we sold Y more; expenses were down by Z because we lost three people in headcount.’”

How should revenues be broken out? (14:12)

Gina: “By number of products sold, pricing, number of customers; whatever metrics that are core to your business. Companies that can do that generally have a good finance department.”

What are some common missteps Colonnade sees in accounting practices of middle market companies? (16:40)

Gina: “The finance department is looked at as a cost center.” Owners keep the books themselves or use a part-time bookkeeper. When companies don’t hire a CFO, there’s a potential problem.

What are some other missteps management can make when getting ready to sell their company? (18:00)

Jeff: “When the CEO is the master of everything. He’s the head of sales, he’s the head of marketing, he’s the head of IT sometimes, and in a lot of cases, he or she is the CFO. That’s a problem because an investor could come in and say, ‘Well, I’m not going to pay $50 million for this one guy or this one woman. Where’s the team?’”

When do you know that a company has the infrastructure to be sold? (18:35)

Jeff: “The real enterprise value gets built when you say, ‘This is a business that is going to be my legacy, but I don’t need to be here as the CEO or the founder. I built this business. I built out a team. The finance function is all built out. The marketing function is built out. The sales function is built out. This business runs on its own. And so if you want me here or not, that’s fine, but my team is really more important than I am.”

Why does a company wanting to be sold need a CFO? (19:00)

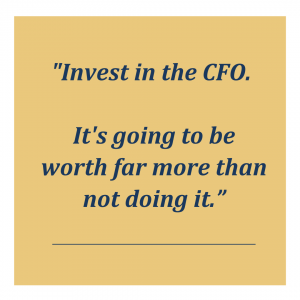

Gina: “Without a CFO, when a buyer comes in, they will do a negative adjustment to your historical financial statements to fill that role. That CFO role will be built into your valuation regardless. So invest in the CFO. It’s going to be worth far more than not doing it.”

What is the difference between GAAP and cash accounting? (20:22)

Gina: “Here’s the non-CPA’s way of explaining GAAP. Under GAAP, the timing of your revenues and expenses need to match, and they need to also match the timing of your liabilities, which means if you are selling a service that is a service for six months, you receive the payment upfront, the revenue upfront, you’re going to have to recognize that revenue over six months.”

What is an example of GAAP accounting vs. cash accounting? (21:00)

Gina: “ A common example is payroll. Accruals should be done for payroll. Let’s say you pay your employees every other Friday. The month doesn’t always end on the fourth Friday, so you end up having to pay in the following month, let’s say the Wednesday the following month. (When you pay in the following month) you’re paying for the prior month’s work. You need to do an accrual for that payroll so it matches the month in which it occurred. So accruals need to be done under GAAP and revenue needs to be recognized in line with what the services or the products provide.”

What industries can use modified cash accounting? (21:36)

Gina: “We work a lot in the F&I (Auto Finance and Insurance) and administrator space. (These companies) can be sold on a modified cash basis. But that doesn’t happen in all industries.”

How does modified cash accounting work when selling a business in the F&I or administrator space? (22:16)

Jeff: The important thing is understanding the difference between the two accounting processes or procedures. In the cases where it’s beneficial to the clients to present themselves on a cash or a modified cash basis, we’re certainly going to do that to maximize value. There has to be a spreadsheet that says, here’s the audit according to GAAP, and here are the cash financials that we want you to value the company on, and here are the adjustments we’ve made to get there, and it has to be logical and make sense and be consistent.”

Gina invites Joe Kaczmarek, an expert in audit tax and consulting services, to share his perspective on due diligence accounting aspects.

What is the difference between an audit and a sell side Quality of Earnings (QOE)? (24:19)

Joe: An audit is to go back and verify information at a point in time. We’re validating the accuracy of your balance statement and your income statement. When we do a quality of earnings (QOE) report, we’re really stripping out one-time expenses, one-time revenues, and coming down to a real accreditable earnings number on a cash basis. From a quality of earnings perspective, it’s also much broader.”

How many years back should an audit go? (27:02)

Joe: “What I typically say is, ‘If you want three years in the marketing documents, it typically presents the best if those are all audited.’ (Three years). But more importantly than how many years is having a firm that really understands the industry and is really nailing down those things that could come up in diligence.”

What are the bare minimum processes and procedures a firm should have in place before they go to market? (28:02)

Joe: “The big thing is having a CPA on staff and having that person really understand what’s required. We like to see monthly financial statements, on not only a cash basis but an accrual basis, a GAAP basis.”

What else should companies thinking of selling consider? (28:34)

Joe: “investing in your financial reporting group. That’s not something that’s providing revenue so it’s often overlooked. You really need to have the infrastructure there to be able to report and provide the information necessary to go through diligence.”

How quickly should a company be able to close the prior month’s books? (29:07)

Joe: “It really depends on the complexity of the organization and the systems they have in place. It can take two days to two months. (However,) those companies taking two months realize very quickly through this process that that’s not going to be adequate (fast enough). If it’s a private equity group coming in to acquire them, they’re going to need reporting on a monthly basis that’s going to be out within a week or two from the month-end or the year-end.”

What is your view on QuickBooks? (30:36)

Joe: “Depending on the industry that you work in, Quickbooks may be adequate. QuickBooks could be fine for smaller companies and midsize companies. But you’ve got to realize what the limitations with QuickBooks are (such as controls, access, and integration).”

How should companies account for a PPP loan? (32:40)

Joe: “There is going to be a portion of it that’s going to be forgiven, if not all of it. You should record it as debt. Then as you get approval for that forgiveness, that’s the point in time when it should flow through your income statement for GAAP purposes. If you look at a transaction, that’s one of those one-time items that will most likely be backed out, and I would say that’s non-operating revenue, so it should be down below the line.”

What’s one piece of advice you would give a company that’s about to go through an M&A process? (33:47)

Joe: “Engage a reputable firm to conduct sell-side due diligence. Sell-side due diligence firms will dig into the company’s financial information and figure out where there may be issues. If identified issues are likely to be deal-breakers, then the company will need to pause the process until the issues are fixed.”

Featured guest bio and contact information:

Joe Kaczmarek

Email: joe.kaczmarek@rsmus.com

Joe Kaczmarek services as the National Fintech leader at RSM. In this role, he is responsible for driving the firm’s strategic objections in fintech, while assisting traditional financial service clients with their digital transformation. Joe also leads RSM’s specialty finance practice for the Great Lake Region. Joe has expertise servicing fintech and online lenders, direct to consumer lenders, sales financing lenders, purchasers of automobiles and other retail installment contracts, rent-to-own companies, title lenders, purchasers of distressed debt, mortgage originators and servers, and various types of commercial lenders. Joe has vast experience providing and supervising audit, consulting, and risk management services to entities ranging in size from startup companies to international organizations. Joe also has extensive experience in transaction advisory services working with private equity groups, venture capital firms, and clients. Joe earned his bachelor’s degree and MBA from Eastern Illinois University.