Jeff Guylay interviewed on the Monitor Daily Podcast

Three Key Questions for Equipment Leasing Firms Considering an M&A Transaction

I was honored to appear with Rita Garwood on the Monitor Daily podcast this month. This article is based on that interview, and you can listen to our discussion by clicking the link posted at the bottom of this article.

Our discussion focused on how smaller independent equipment finance companies can take successful steps to benefit from today’s highly favorable Mergers & Acquisitions (M&A) market.

As the leader of Colonnade Advisors’ specialty finance practice, I love assisting independent owners who are considering selling all or a portion of their business.

In this interview, I answer some important questions I’m often asked by company owners, including:

- Why would Independents benefit from a merger with a bank?

- What are some of the drawbacks and considerations of a bank merger?

- What are the next steps for companies considering going to market?

Why Would Independents Benefit From a Merger with a Bank?

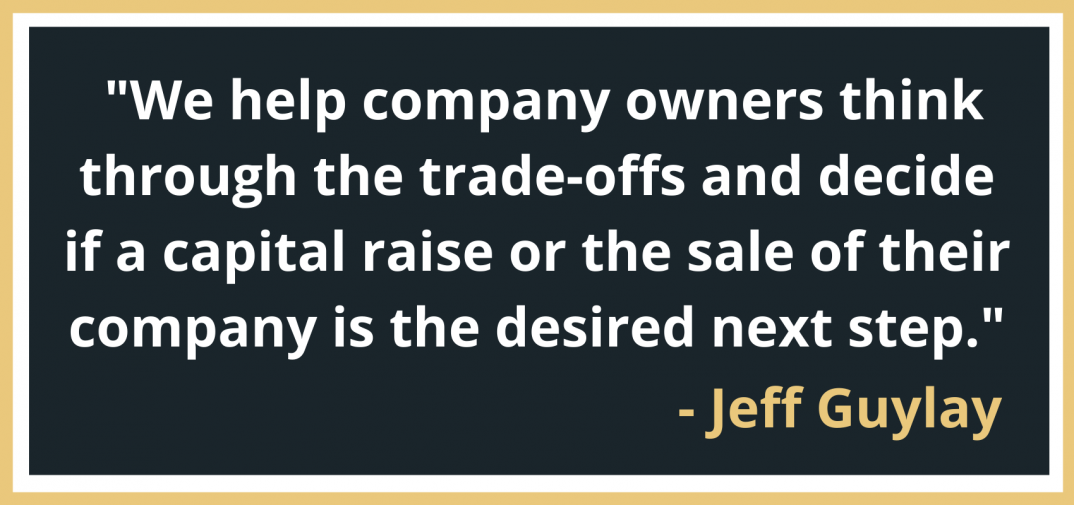

We spend a lot of time working with company owners even before they become clients to get everyone crystal clear on their objectives. We help company owners think through the trade-offs and decide if a capital raise or the sale of their company is the desired next step. If they want to go to market, we first help them to get mentally ready for a transaction.

Independents are known for their agility and ability to achieve rapid growth without the regulatory hurdles faced by banks. However, banks have competitive advantages related to access to and cost of capital.

With this access to and cost of capital, independents can be more competitive and grow more quickly. The larger entity benefits from longevity and sustainability. Banks bring large balance sheets with low cost of funds, which can supercharge an already strong leasing platform. Banks can bring distribution and diverse resources. These advantages mean that rolling an independent equipment finance company into a bank can prove to be a lucrative win-win strategy.

I generally think of banks as a natural resting home for specialty financing businesses and equipment finance businesses. But a transaction with a financial sponsor or private equity firm can serve as a stepping stone to the ultimate sale to a bank or other financial institution.

What are Some of the Drawbacks/Considerations of a Bank Merger?

Banks are subject to regulatory oversight and scrutiny. Operating within a bank is quite different than being independent, as autonomy, flexibility, and agility are reduced with institutional ownership.

Independents must also commit to planning and making investments necessary to be part of a large regulated financial institution. This commitment is a considerable undertaking.

Planning can be anything from talking to competitors and peers, working with consultants, building out a plan, and hiring advisors like us. We also see the need to build up the management team, create succession plans, and put in place solid policies and procedures. We ask our clients to think about what sort of discipline a third party would impose on you, and start doing it yourself.

We see that independents must also invest not only in people but also in systems and technology/ infrastructure. This is expensive and time-consuming; however, these investments serve to build enterprise value, which can pay off handsomely in a transaction.

When it comes to technology, which I talked about quite a bit on the podcast interview with Rita, you want an IT platform that can leverage the best of all the third-party and proprietary elements. We find that firms that invest in data acquisition and management ultimately command the highest multiples in a transaction.

We work with consultants like Bob Rinaldi who can help you pick the best lease management platform or outsource servicing firm and then integrate with the best data warehouse solutions and management reporting dashboard. These technology solutions empower your employees from sales and marketing to the CSRs and everybody in between. When it comes to technology, we advise getting everyone involved in utilizing the data across the organization. This way, data integrity improves naturally and is part of the fabric of the organization, assisting everyone in managing the business more efficiently.

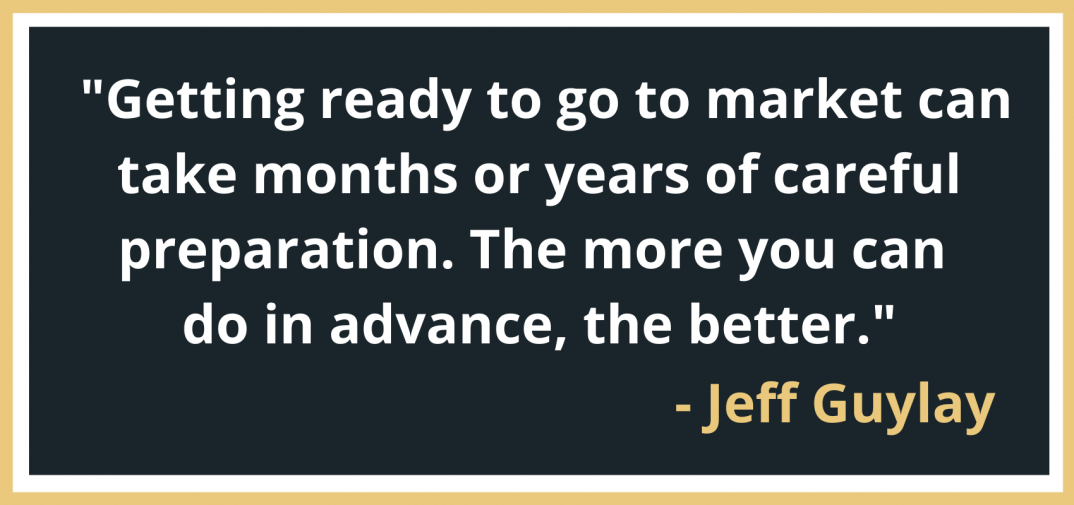

Getting ready to go to market can take months or years of careful preparation. The more you can do in advance, the better. The more prepared you are, the better price and terms you’ll ultimately get in a transaction. We recently worked with one of our bank clients to acquire an independent lessor that had invested heavily in recent years to upgrade its data warehouse and reporting capabilities. They had built an impressive dashboard that helped them manage the business. As a result, they commanded a high multiple and a high price in the market.

We enjoy getting involved in helping companies quantify what the above looks like and whether or not it is worth it. We enjoy working with companies that are ready to sell as well as companies that are in the ideation stage about going to market.

What are the Next Steps for Companies Considering Going to Market?

We are experts in helping our clients get tactically ready for a sale. That generally involves being what we call “bank ready” – whether you’re selling to a bank today, entertaining a transaction with a private equity firm, or even staying independent. All this preparation serves to build enterprise value.

When we work with clients to get ready for a sale, we take them through a fully vetted four-step process that we’ve been using successfully for decades.

Our phases are:

- Pre-Marketing

- Go to Market

- Management Presentations / Buyer Due Diligence

- Exclusivity / Documentation

Once you are ready to hire an advisor like us, you want to be ready for internal due diligence. This means working with the advisory team and providing us with information so that we can prepare the confidential information memorandum, get the financial model in place, and detail the growth story. That’s a very fun part of the work that we do. And of course, it builds significant value in any transaction by best preparing the company for going to market.

Conclusion

Banks want to be in equipment finance and leasing. It’s a great sector for them. Being bank-owned can bring significant benefits for finance companies. For owner/operators, there are trade-offs between being independent and being bank-owned. Please feel free to reach out to me if you have any questions about how the factors I’ve discussed in this article and in my interview with The Monitor Daily might affect your decision-making process related to selling your company.

Resources and Links

This article is based on an interview I did with Rita Garwood, Editor in Chief of The Monitor Daily. I am very appreciative of the opportunity to have appeared in this interview. This podcast is sponsored by Orion First and can be found here (20 minutes).

Click here to read Colonnade’s Industry Report on Small Ticket Equipment Leasing and Finance.

A more detailed diagram of our four-step process of selling a company click here.

Listen to Colonnade’s podcast episodes (Middle Market Mergers & Acquisition) on the process of going to market:

EP 001 – Phase one (pre-marketing)

EP 002 – Phase two (go to market)

EP 016 – Phase three (management meetings)

EP 017 – Phase four (the exclusivity phase)

Related Posts: